The FED's dilemma

The FED's dilemma

If you want to receive these newsletters by Crypto Jali directly by mail, subscribe to his newsletter here.

The FED's Dilemma

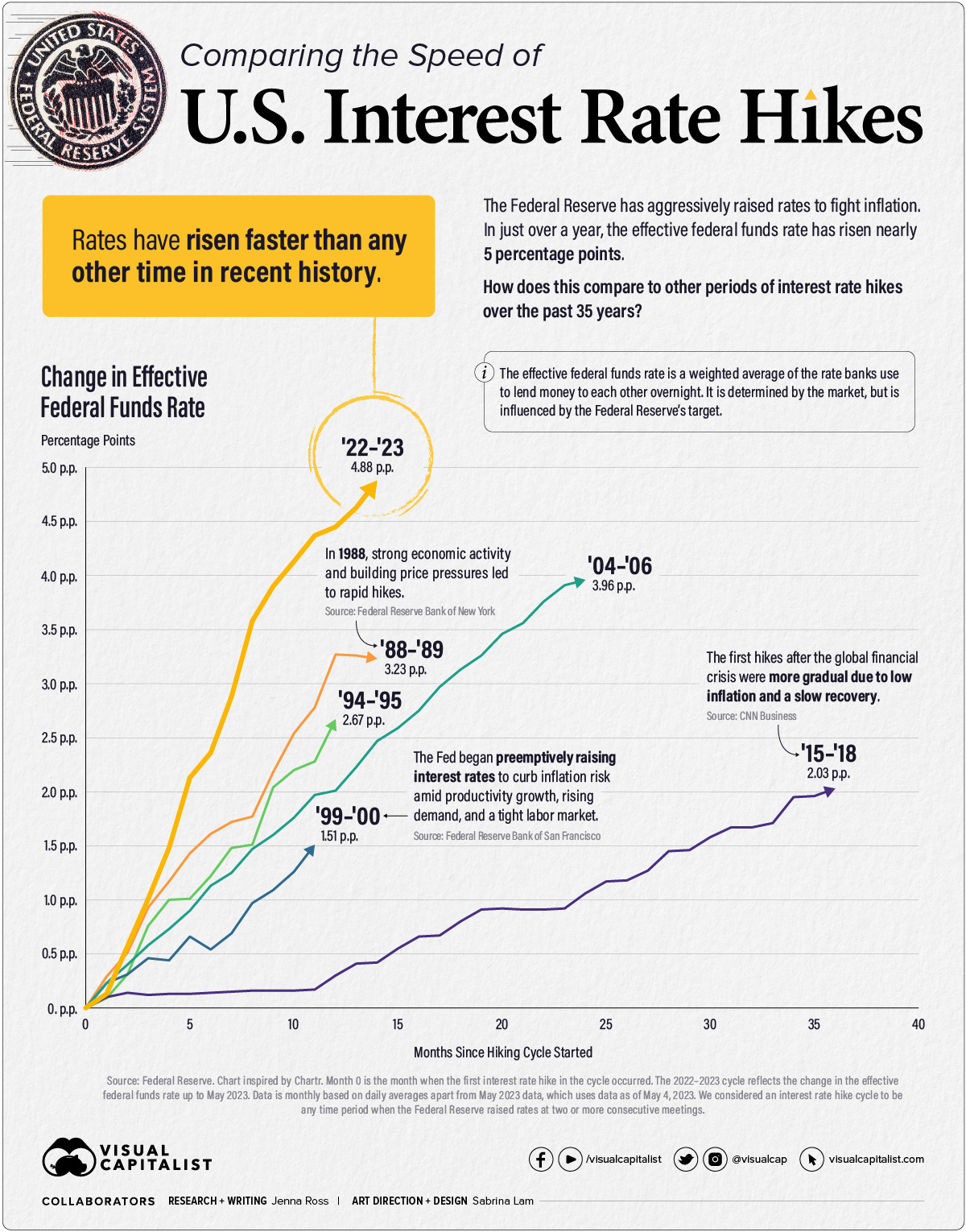

Never before has the Fed raised interest rates so aggressively and rapidly (see image). In just over a year, interest rates were increased by nearly 5%. Why? Because of high inflation.

It is the Fed's task to keep inflation around 2%. But as we know, inflation has been much higher in the past year, peaking at 9.1% in the US. In response, the Fed raised interest rates harder than ever before. As a result, inflation has now been reduced to 4.9%. A step in the right direction, but still well above their target. And that's why the Fed finds itself in a dilemma, which I'll explain below.

A decade and a half of free money

Since the end of 2008, interest rates have been steady around 0%, with the exception of a short period of small rate hikes between 2017 and 2020. For 15 years, banks and financial institutions have grown accustomed to low rates and cheap money. Therefore, this fastest rate hike in Fed history is causing problems for banks.

What’s the main issue? Banks have a significant amount of low-yielding loans, mortgages, and bonds on their balance sheets. Now that rates are so much higher, the value of those loans, mortgages, and bonds has decreased significantly. According to estimates, the paper losses on banks' balance sheets amount to at least $1.7 trillion!

As a result, many banks are no longer sufficiently liquid. This leads to fear among customers, who withdraw their deposits. For this reason, several banks have already collapsed in recent months:

- Silvergate Bank

- Silicon Valley Bank

- Signature Bank

- Credit Suisse

- First Republic Bank

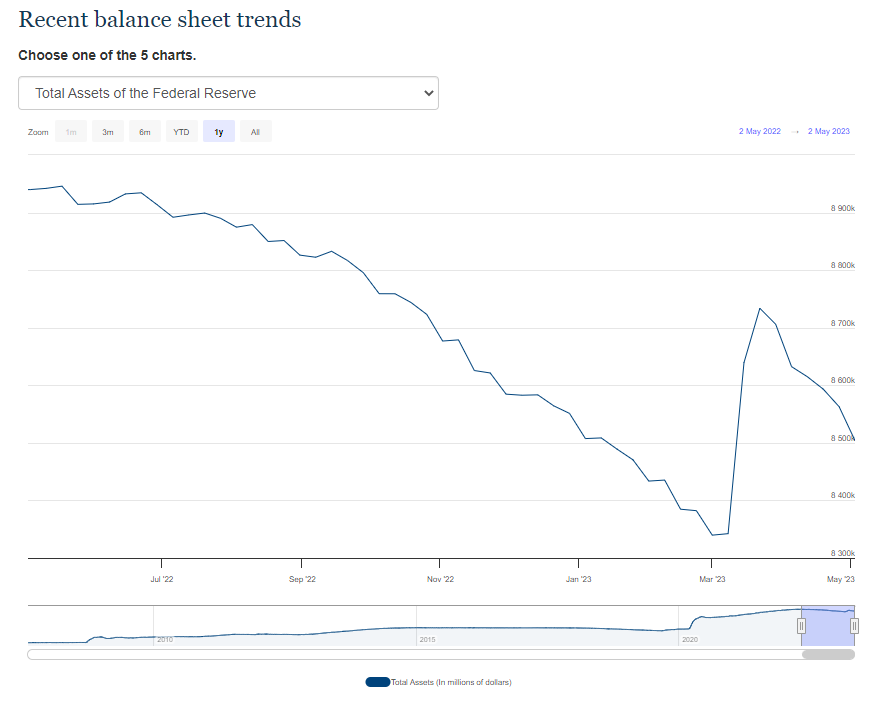

Most of these banks were rescued by the FDIC, the US equivalent of the European deposit insurance fund. The consequence was that the Fed had to significantly expand its balance sheet between March 7 and March 21, while they had originally planned to shrink it to curb inflation. Due to this reaction from the Fed, being counterproductive to reducing inflation, Bitcoin rose by over 40% and gold by more than 10% during the same period.

As long as rates remain high, more and more banks will face similar problems. Remember, the total paper losses amount to more than $1.7 trillion. To provide some relief to banks, the Fed could lower interest rates. However, that would lead to higher inflation.

Therefore, the Fed finds itself in a dilemma. If they lower rates to give banks some breathing room, inflation rises. If they keep rates high, more banks will collapse. And then they have two choices:

- Guarantee all bank deposits. For that, they would need to further expand their balance sheet, which again, would lead to higher inflation.

- Let the banks, and consequently the engine of the US economy, fail and don’t guarantee deposits. From the past few months, it's evident that this is not their preferred option, as the FDIC (sometimes indirectly) guaranteed every dollar in a US bank.

The FED dilemma seems to be a blessing for Bitcoin (and gold). Regardless of the choice the Fed makes, it will likely result in higher inflation, forcing investors to seek for stores of value.

In my article "$25k Bitcoin incoming?" I wrote that I considered it likely for Bitcoin to correct to $25k before heading towards $32k. I still believe that. But more importantly, I think the unique and complex situation the Fed finds itself in will lead to a new bull market for Bitcoin.

$40k per Bitcoin is, in my opinion, the next stop after we reach $25k. And I wouldn't be surprised if Bitcoin gets close to its old all-time high by the end of this year.

This is Bitcoin's moment to shine. This is why Bitcoin was created.

If you want to receive these newsletters by Jali directly by mail, subscribe here.